A Dollar Bill is Always Worth One Dollar, But …

The Stage: US Congress Amok

In our last edition, we took prominent notice of the fact that Fitch Ratings, Inc. had become the 2nd of the 3 major debt rating agencies to lower the US Government’s once impeccable credit rating. Fitch’s explanation of its downgrade very candidly zeroed in on the current US Congress’ constant and continuous instability, intransigence and (implied) ineptitude. The sheer disorder produced by narrow, factional priorities appears to have deteriorated Congress’ core systems for performing its Constitutionally mandatory business.

Now the Congress has pulled off yet another panicked (2AM Saturday morning) rescue from the threat to put a large chunk of the government’s operations on ice. In so doing, they funded only six of the twelve departments for the already half-expired fiscal year. Also left dangling in controversial limbo are costly, sensitive supplemental funding bills for two US proxy-wars, both of which urgently beg for large new shipments of critical arms and tech tools.

The Course: Deficits, Debt and Dollars

This year’s hit and miss Congressional budgeting is merely the latest one. It is clear that budgeting of the “discretionary” one-quarter of total federal spending is what gets the majority of members’ time and attention; most years, little is said and done about revenues. Other than relatively brief periods of economic depression and not-so-brief major wars, it is economically impossible for a government to levitate above decades of continuously compounding budget deficits. The US appears to be unavoidably on course to test that deficit-compounding roadblock.

The engine of this scenario is a worldwide pool of willing government and private lenders who believe their risk exposure in owning US debt obligations is not only negligible, but the safest available investment on the globe. The facility for its continuation is the sought-after medium of exchange… the US Dollar… which all lenders continue to have faith will safely sidestep the consequences of an overleveraged scenario that simply does not compute.

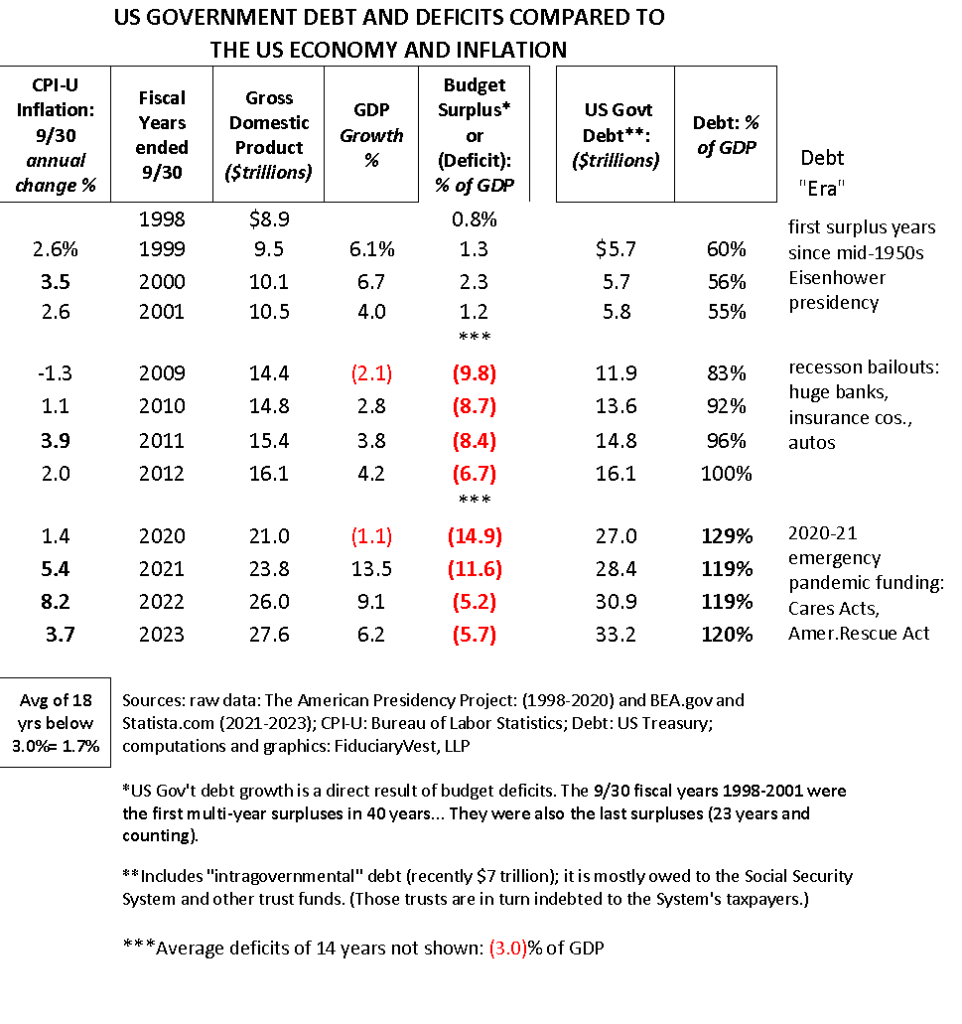

We have assembled all the numbers to paint the picture that displays not only the current US debt situation, but also the path that got us here. As a starting point, we selected the four-consecutive fiscal years period 1998 – 2001, 23 years ago, when the US Government booked a surplus. It was a highly significant period, as the waning years of the 20th Century saw an economic revolution – on a scale that was equivalent to the invention of the wheel: an explosion of economic capability and efficiency made possible by widespread business implementation of the Internet. Once again, it was the US that started this global technological revolution.

There is apparent growing concern among trading nations, most notably China, India and Middle Eastern countries, about endless creation of US Dollars and annually spending of trillions of those “red dollars”. Domestic economic growth increases tax collections, but tax growth is consistently falling further behind Congress’ undisciplined spending growth.

During all of the 21st Century to date, the US Government’s method of funding numerous new “programs” that are politically useful is as simple as this: Treasury issues $trillions more debt; the Federal Reserve creates more dollars with which to buy that debt and the result is a surging existence of new dollars unmatched by increased tax collections; hence, more and larger deficits that are growing faster than the overall economy.

The Gold Role

A robust, international trade network necessarily requires a universally recognized medium of exchange. For thousands of years gold, one of 94 natural elements, was that widely valued medium because of its unique set of attractive characteristics… It is relatively rare, indestructible, easily divided, transportable and uniformly prized among all civilizations. But gold used for goods and services transactions grew exponentially and that became awkwardly inefficient.

To cure its handling problems, trade-focused nations began to substitute gold-backed paper notes… the notes were official, government-printed promises to settle each purchase/sale with a specific amount of physical gold. People came to fully trust the engraved promises on the paper notes. Hence, in every meaningful way, the printed paper notes became “money” that was “as good as gold.” History: Paper money in evidence of precious metals can be traced back to the promissory notes of ancient China, Carthage, and the Roman Empire, over 2000 years ago.

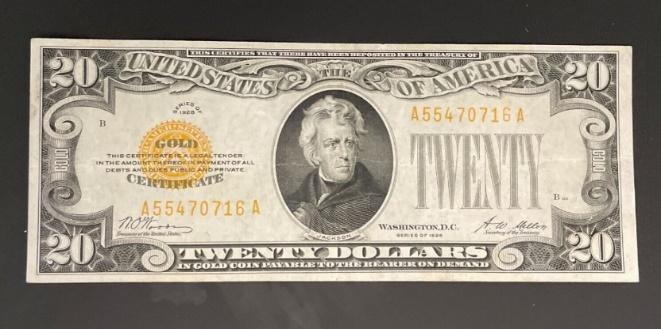

Here is a US 20-dollar Gold Certificate issued in 1927. At the top and bottom edges, it states: “This certifies that there have been deposited in the Treasury of the United States of America TWENTY DOLLARS IN GOLD COIN PAYABLE TO THE BEARER ON DEMAND”. For nearly 100 years until the 1930s, gold was priced at $20.67 per ounce, so this paper Gold Certificate could be turned into almost 1 ounce of gold on any business day of the week.

If you could and wished to convert this twenty dollar note into gold today, 97 years after it was issued, you would have to pay 120 of them to receive 1 ounce of gold (currently market-valued at about $2,400).

Besides December 7, 1941, another infamous date in American history was April 5,1933—the day President Franklin Roosevelt issued an Executive Order to bring about the confiscation of private holdings of gold and paper gold certificates held by the American people… and the order required full compliance within 3 weeks! The reasoning behind the order was an alleged pattern of gold hoarding that was believed by the president’s advisors to be frustrating his massive Great Depression-fighting programs. Because the federal government then owned such a large chunk of all gold, it was able to fix the price per ounce, which it did in 1934, at $35 (almost 70% higher than the longstanding $20.67 confiscation price paid to fuming, gold-holding citizens only one year earlier).

After the two World Wars, the UK and Europe (including Germany) required an unprecedented level of international economic assistance and trade in order to recover, reconstruct and renew from their widespread devastation. Thus, after almost 100 years, Great Britain’s Pound Sterling currency was no longer capable of continuing its reserve status. So, in July 1944, representatives of 44 countries met at Bretton Woods New Hampshire and agreed to designate the US Dollar as the new reserve currency among and between all of them. They also specified that one dollar would permanently be convertible into one ounce of gold at a fixed price of $35 per troy ounce.

That currency management regime worked until August 1971, when, during a weekend at Camp David, President Nixon was warned by a group of economic advisors that the open-ended creation of more and more dollars had made the US promise to sell bulk gold to anyone, at the exchange rate of 35 paper dollars per ounce was a bargain for dollar-holders, at the expense of the US Treasury. So, two days later Nixon issued a(nother) Executive Order proclaiming that the dollar was simply no longer redeemable in gold.

Simple, indeed. That action was in fact an overnight US Government default on its 27-years-old gold exchange promise. The automatic result was: (1) explosive re-valuation of gold[1]… now that gold’s dollar-value was free to increase in direct proportion to the amount of new dollars and, (2) the valuation of all of the world’s local currencies soon began to freely float, versus the US Dollar and among themselves. Three years later, President Ford formally removed Roosevelt’s 41-year-old prohibition against private gold ownership. Next, after 25 years of this higgledy-piggledy currency morass, the European Union was born, and it issued a single currency backed by the economies of 20 nations. Like the dollar, the Euro is a fiat currency which means that the number of euros in existence is unlimited and it has no physical backing.

How Will the Dollar Face Emerging Challenges?

The US Dollar’s continued super-status as the globally recognized reserve currency is presumed, but not assured. Factors that might make any dollar-replacement difficult are: (1) sheer process-inertia that would confront major change, (2) the stability of the US Constitution’s, legal and political respect for property rights, (3) the US’s extensive societal operating structure, (4) the US’s governmental design strength and integrity and (5) the US’s vast, well-funded entrepreneurial structure and spirit. If this paragraph captures the world’s reasons for favoring dollar reserves, then it is worthwhile to review each of them to assess their prospectively continued strength.

At the outset of Russia’s invasion of Ukraine, the US froze Russia’s access to its roughly 300 billion dollars held as trading reserves in US banks. According to the Financial Times, December 2023, The United States has proposed that a working group from the Group of Seven (G7) major industrialized nations explore ways to seize Russia’s frozen dollars. Apparently, such a seizure would be used to fund Ukraine’s war effort against Russia. But a number of international bankers have made known their belief that such a confiscation and re-purposing of Russian-owned dollars would significantly weaken the dollar’s global support for its continued status as the world’s reserve currency.

Grinding out new currencies

As noted above, the US Government’s debts to investors around the world recently suffered two independent, insulting credit downgrades, but there are no similar watchdog agencies that rate currencies; hence, the US Dollar, for now, still sits atop all other world currencies. We noted in an earlier article that a widely dispersed group of nations (BRICS) that have extensive petroleum reserves and/or super-large populations have formed a trading alliance that uses their respective currencies to replace the US Dollar for trading among themselves. Those trades represent a sort of limited commercial partnership. However, because the group includes China, Russia and India, it is far too early to conclude that their organization will remain limited. It does seem that they have an immediate need to launch a common currency; if so, it would be tied to a widely accepted “valuation-constant”… perhaps gold, perhaps Bitcoin.

Cryptocurrencies Moving In?

In addition to gold, there is another medium of exchange that is also a commodity, the value of which will reflect societal price inflation.

The penultimate stage of commodity supply vs demand: This year, the grandfather of cryptos, the Bitcoin block-system will see a mechanically mandated “halving event” in April that will cut in half the number of new Bitcoin that can be mined. Up to now, there have been 3 such halvings and, in each case, the dollar value of Bitcoin soared. Bitcoin’s block-by-block creation architecture has a maximum (forever) supply of 21 million Bitcoin, of which 19.22 million have already been mined as of this month. The Real market has jumped into the crypto pool. In January of this year, the SEC issued approval of several major investment firms to

startup and operate crypto ETF pools. This large market entrance group will offer easy, simple access to any and all investors, large and small. Predictably, near term supply and demand will dampen the sometimes dramatic crypto price volatility and also tend to push the price higher and higher, as halvings occur more often, even if the demand side is not growing.

In Summary

KING DOLLAR ERA: After World War II was fought on the soil of many nations, those nations readily agreed that the US was the ultimate victor which had re-configured its entire society and economy in order to develop, build and deliver high quality fighting equipment, well-trained troops and effective command structure that would turn the war in both Europe and the Pacific into the defeat of the two attack-nations that started it. Indeed, the developed world of 1944 had only one choice as to which currency would be the consensus medium for international commerce. And post-war consumer demand for goods in the US economy rocketed to unprecedented heights.

Before the end of the century, both Europe and Japan had evolved into thriving, growing renovation and financial strength. To maintain orderly commerce, there was still a need for a common exchange medium. The US Dollar was still fit for that job. At the end of the century, along came the US Internet revolution. The result: US economic prowess was re-ignited and it plowed headlong leadership into the 21st Century on the heels of a refreshing 4-year set of annual US budget surpluses (fiscal 1998-2001).

SINCE: The US Government has run continuous annual budget deficits. The new Congressional norm is to adopt open-ended annual deficits whether or not there is underlying cause. The consequence is, of course, an accumulating debt that cannot be set aside.

Footnote: A comprehensive Brown University/Watson Institute study puts the total of post-9/11/2001 Afghanistan/Iraq war spending at a whopping $8 trillion.

The US set a costly fire inside the world’s economies via a mammoth 2008 collapse of US’s private sector lending and debt facilities. That breakdown caused both the Congress and the Federal Reserve to make unprecedented bailouts that created major deficits, more debt and a weakened dollar. In 2020, the Covid-19 pandemic brought most of US society to a halt for about half of that year. Congress’ reactions to those two economic crashes directly resulted in sudden, massive deficits in both 2009-2012 and 2020-2023 periods. The accumulated US Treasury deficits during those two 4-year periods has jumped the debt-to-GDP ratio to a record high of 120% in 2023 from around 55-60% before 2002. There is no generally accepted limit for the debt/GDP ratio. But one of the trailing no-no indicators is flagged when the interest on that deficit-driven debt exceeds the entire annual budget allocation to the Defense Department. This year, we have reached that point, driven by sharply rising interest rates on Treasury notes and bonds.

(1) Congressional failure to adopt budgets and (2) its predilection to pour unlimited trillions of dollars into nearly every war situation that comes along, while (3) underwriting losses in some industries have collectively introduced serious questions about the US Dollar, questions recently reacted to by two of the three credit rating agencies. In addition, last year there was a series of major US bank failures which the Treasury decided to cover and relax ironclad FDIC limits on its insurance responsibility, i.e., bank shareholders should have, but didn’t absorb those losses.

Finally, trading volumes and newly available investing vehicles indicate that there is real logic behind an apparently growing preference for holding gold, silver and Bitcoin instead of dollars.

Commentary

Commentary was prepared for clients and prospective clients of FiduciaryVest LLC. It may not be suitable for others and should not be disseminated without written permission. FiduciaryVest does not make any representation or warranties as to the accuracy or merit of the discussion, analysis, or opinions contained in commentaries as a basis for investment decision making. Any comments or general market related observations are based on information available at the time of writing, are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm, and should not be relied upon as a basis for making investment decisions.

All information contained herein is believed to be correct, though complete accuracy cannot be guaranteed. This information is subject to change without notice as market conditions change, will not be updated for subsequent events or changes in facts or opinion, and is not intended to predict the performance of any manager, individual security, currency, market sector, or portfolio.

This information may concur or may conflict with activities of any clients’ underlying portfolio managers or with actions taken by individual clients or clients collectively of FiduciaryVest for a variety of reasons, including but not limited to differences between and among their investment objectives. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decisions.

We welcome readers’ comments, questions, criticisms, and topical suggestions about our Commentaries, which always contain a mixture of researched facts and conclusions about their impact. We diligently strive to avoid controversial, or partisan views. However, our conclusions clearly cannot always align with our readers’ various interests and personal points of view.

The research topics and conclusions herein are not “FiduciaryVest, LLC viewpoints,” nor are they attributable to its individual employees.

Investment Risk

FiduciaryVest does not represent, warrant, or imply that the services or methods of analysis employed can or will predict future results, successfully identify market tops or bottoms, or insulate client portfolios from losses due to market corrections or declines. Investment risks involve but are not limited to the following: systematic risk, interest rate risk, inflation risk, currency risk, liquidity risk, geopolitical risk, management risk, and credit risk. In addition to general risks associated with investing, certain products also pose additional risks. This and other important information is contained in the product prospectus or offering materials.

[1] 53 years in the rear-view mirror… $35 gold fixed-price per ounce in 1971 has free-floated to $2,400 in early April 2024. That’s a price multiple of 65x. Meanwhile, the Dow Jones Industrial Average was 885 in 1971; today it is above 39,000 which is just over a 44x multiple. [Neither gold’s price, nor the Dow index includes dividends or interest.] A discount for the above growth numbers…. the CPI-U inflation index went from 40.5 in 1971 to 304.7 in 2023, a multiple of 7.5x.