Now Batting in the Bottom of the 9th…GREECE

(Pipe)Dreaming of Drachmas

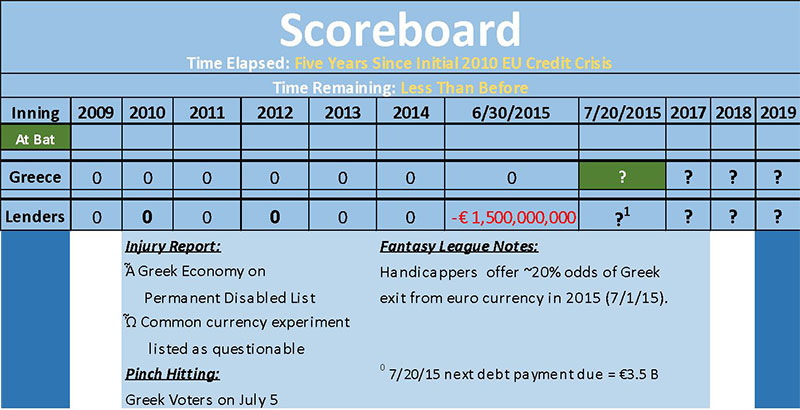

Greece is a relatively tiny economic player globally, with a ~$240B GDP (measured in USD), about half that of Poland. Critically though, the cradle of western civilization has amassed total debt1 greater than its GDP, above levels that common sense (and even professional economists) consider repayable. Given the market volatility precipitated recently and by similar events in 2010 and 2013, we offer below a brief recap of the background, changes in context since prior Grexit -related (Greek-euro-exit) market tremors, and additional implications.

While not irrelevant (especially to the lenders), the nominal amount of Greek borrowing that might get rescheduled / forgiven is also small in relation to global capital markets, though the absolute size of the “haircut” has been less the market’s concern. Rather, since 2010, an always-looming global financial bogeyman has been the possible unintended consequences of a Hellenic write-down or default, such as:

- The destructive influence (capital impairment, earnings contraction and the associated transmission to even slower macroeconomic growth across Europe) of a Greek default on counterparties – especially banks – forced to recognize losses.

- The potential for financial “contagion” as either or both of the above scenarios recreate the conditions of the 2008 Financial Crisis, A so-called European “Lehman moment.”

- The setting of precedent (or roadmap) for other, larger but similarly situated European economies (Portugal, Spain, Italy) to beg forgiveness or depart.

The circumstantial change since 2010’s / 2013’s capital market “risk-off” tremors centers around contingency planning, and risk management, more on the side of Europe than Greece, given their respective positions. Spurred to action by 2010’s events and subsequent slow growth and deflation concerns, Europeans have shifted Greek liabilities onto marco institutions like the EBC and IMF, which have larger resources (“whatever it takes,” according to ECB president Mario Draghi), creating something of a firewall on immediate panic related to non-payment or ultimate exit from the euro. They also opened the liquidity spigot earlier this year, with a massive quantitative easing program, backstopping exposed lenders and thereby removing much of Greece’s negotiating leverage. And of course all of this is no longer a surprise as it was in 2010, very much on the heels of 2008-2009 market panic and recession. Witness global markets’ more muted reaction/recovery pattern of late relative to 2010 and 2013. (So far; there are some august opinions2 that we’re far from out of the woods).

The sheer quantity of Greece’s debt ensures its polity faces a troubled future absent an outright debt forgiveness plan by Europe’s leaders (which currently seems unlikely3). Whether in or out of the euro, significant changes are afoot for Greeks – improved tax compliance (avoidance / non-payment is reported to be a badge of honor among many citizens), greater economic productivity, pension and labor reform and any and every measure that will help the economy grow to provide resources to repay – even a restructured debt load will require repayment (someday). In this light, the precedent issue remains a concern, but is likely less immediate if greater Europe refuses to negotiate with a Greece that some commentators have described as “taking itself hostage.” Few additional countries seem poised to embark on such a Spartan path before examining empirical evidence that the lot of average Greeks is better off a few years down the road.

The next step involves a hastily drawn plebiscite – they invented democracy after all – to be considered by Greek voters on July 5. Euro-leaders have indicated they will view a “no” vote4 as tantamount to Greece opting out of the euro common currency. (Perhaps they never should have gotten in, but that’s a story for another day.) If this is the expressed will of the demos, presumably Greece has teed up the financial and printing infrastructure needed to revive the Greek drachma5, the same currency with which a certain Jewish carpenter in ancient Palestine paid temple tax. But the drachma will be no miracle for modern Greeks, since it will be highly devalued relative to the world’s non-defaulted (as of yet) currencies. The Greek debts must be repaid in the currency in which they were borrowed, largely or exclusively euros. This has been the Greek challenge all along – they borrowed in a currency they cannot print, manipulate, or inflate to make repayment easier (a la the US, Japan, and EU).

Seemingly every other (not each one, but every other one) commentator has been tempted by the Greek drama metaphor, and we too take the bait. There will be no deus ex machine: In substance Greece will default, regardless of the form, whether in euros or drachmas and despite the sturm und drang from here to there. The debt is just too large to ever truly repay. If you are tempted to schadenfreude (sorry, the Germans are so prevalent in Europe’s debt negotiations that Teutonic words keep slipping out), consider Larry Summers impolitic utterance of a few years ago on the United States fiscal condition. “Without the printing press, we’re Greece.” Happy Fourth of July?

- Estimated at 1.75X GDP. https://graphics.wsj.com/greece-debt-timeline/ To rein in our potential for American smugness (tsk-tsk, those profligate Greeks), consider that the US at 80% debt-to-GDP is flirting with Harvard economists Rogoff/Reinhart 90% danger zone level. Counting off balance sheet promises (admittedly possible to renegotiate via Congressional action – please stop laughing) takes the ratio to a decidedly frightening >4X!

- See for example, ‘The Consequences of Greece’s Impending Breakdown’ in a recent (and dire) Larry Summers (who gets our last word, below) Washington Post Op-Ed.

- Almost literally as we are compiling this brief note, news reports from Europe vary related to a possible “deal” to avert a (now further, since they missed a payment to the IMF two days ago) debt default by Greece to those institutions [the “troika”, or 1) European Commission, 2) European Central Bank, and 3) International Monetary Fund] overseeing its bailout / workout. It is a very fluid situation, and of course markets are open and watching, and will adjust to news.

- As in “No,” to the ECB, et al conditions for Greece to free up capital to continue the “friendly” workout to make timely repayments to creditors.

- Greeks presumably also could create an entirely new currency rather than revert to the drachma. In any event, it will for time presumably give off the opposite aroma of Shakespeare’s ‘rose by any other name.’