Q1 2015 Market Commentary

“…we are living in a material world, and I am a material girl…”

– Madonna

[Madonna was the Lady Gaga of the 1980s for you curious Millenials. Speaking of which, for no good reason we can discern, we have it on competent authority that Lady Gaga has 44 million Twitter followers. We agree Ms. Ciccone makes an odd choice for quotation here; what can we say?; we’re ‘crazy for her’.]

Is the Material Girl1 right? Are we, in fact, living in a material world? We ask because “way” back in 1984, the Queen of Pop, a famously shrewd business person,2, seemed a bit confused. She spent most of her hit singing about some form of money rather than things (’the boy with the cold hard cash… ’If they don’t give me proper credit…’ ‘boys who save their pennies…’), in subtle contradiction3 of the chorus and title (her own and the song’s).

The distinction seems pertinent today, because it seems to us that we’re living in an increasingly financial world. We don’t mean to engage in semantics and aren’t preparing a populist rant. This space is by definition dedicated to helping make sense of the investing corner of finance, but it is at least interesting to note that Google searches on ‘money’ / ‘manufacturing’finance’ / ‘making stuff’ yield about the same 3.5X weighting in favor of dollars to do-hickeys.

The Fed sees more data than we do, but maybe the real economy is suffering from neglect by comparison to “high finance.” In a similar vein, our ears perked up when a European hedge fund manager recently confided to us that his dad never understood his dedication to an investing career – “trading pieces of paper” rather than “making something.” Perhaps the elder Dutchman was troubled by that, concerned that in the words of Cyndi Lauper, another 1980s pop-diva, “money changes everything.”

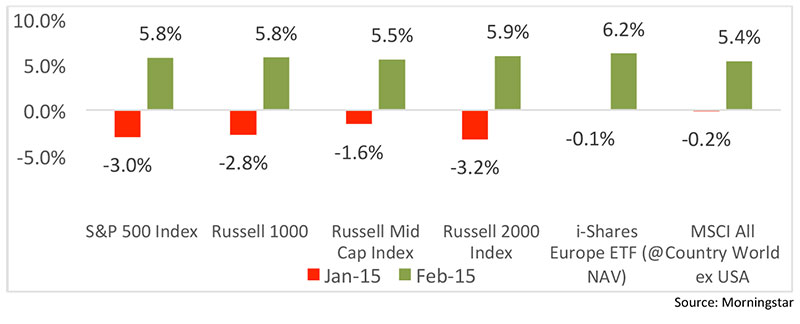

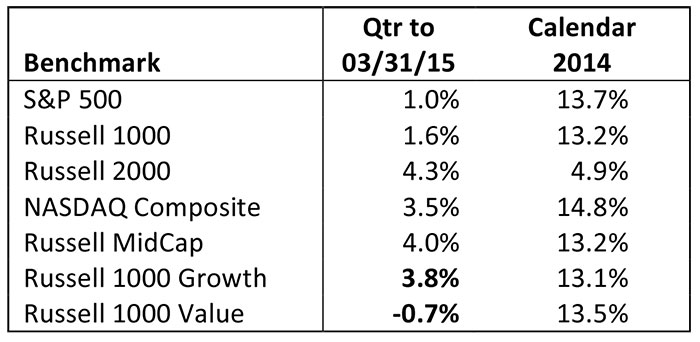

To make the point crystal clear, money surely changed the direction and tone of the financial markets early this year, with 2015 stumbling out of the gate with meager to negative results in January but turning in decent 1Q (and now year to date through April) results.

The difference, one might argue, was that in late January, the financial world made the something it makes best in the post GFC (Global Financial Crisis) world: more money. Not making more money like you and I think about it –

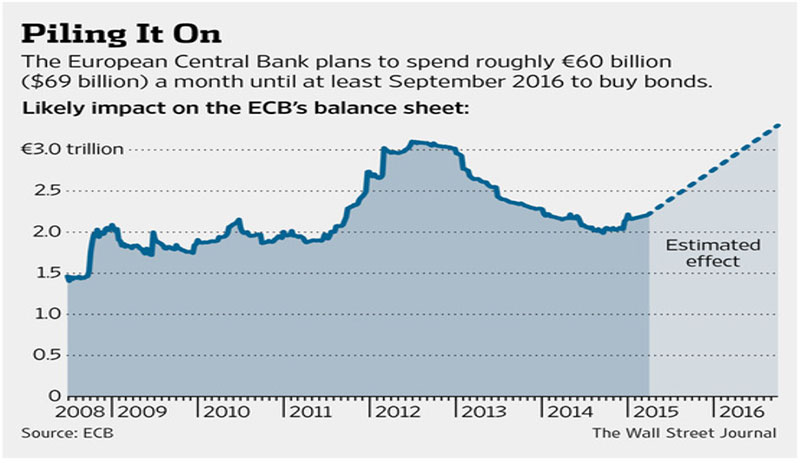

working longer/better/faster – but the way only a central bank can make it: legally, by fiat. Though European Central Bank President Mario Draghi is Italian, his French appears excellent – and so, voilà: the ECB delivered its version of QE4 in late January announcing an unexpectedly large $1.1 trillion bond-purchasing scheme that will last through 2016.5

In fact, the ECB chairman seems so certain of the ascendancy of central banking power and foresight that he said in 2012 “there is no going back to the lira or the drachma or to any other currency. It is pointless to bet against the euro. It is pointless to go short on the euro6.” After his QE launch, he doubled down, indicating that he would say exactly the same today, even as Greece’s (insolvent) government angles for more “pretend and extend” treatment from its global creditors, largely the ECB, IMF, and World Bank. Perhaps Mr. Draghi and his cohorts should consider a twist on the old adage: beware Greeks bearing grifts7.

1Q 2015 Market Results

Marquee Capital – 1985 Material Girl Dress from Video

As far as the financial prediction / talking heads business goes, ‘When Will the Fed Tighten?’ is the Triple Crown, Super Bowl, and “did Tom Brady cheat?” all rolled into one. Ironically, now that the US has curtailed its own QE (in terms of new asset purchases), a Fed Funds rate hike size and timing is the risk most investors are worrying about. (“If they can’t raise my interest than I’ll have to let them be…8”) GDP, jobs, inflation, and oil are sideshows to the great rate query. It may be the most handicapped event since Seabiscuit / War Admiral. Perhaps Madonna should have ‘vogued’ Rita Hayworth rather than Marilyn Monroe for her famous video.

What’s an investor to do as Ben Bernanke and the Wall Street Journal editorial page duel out interest rate hike timing/necessity wisdom in ink/pixels and regional Fed governors send contradictory signals in speeches? When Fed Chair Janet Yellen muses aloud about possibly

elevated stock market valuations? Presumably no Fed Chair goes “open mic night” without thinking about the message. A lot. It surely makes sense to think now about how portfolio rebalancing might be affected, based on which signals and to what degree. Where does your policy call for adding risk exposure when appropriate? Where will you fund it from?

We have no crystal ball on interest rates or advance notice on market downdrafts. Our systematic review of asset classes is giving no current sign of equity retrenchment worthy of pre-emptory rebalancing. But here’s a worthy question to ask amidst the turbulence of interest rate prediction game: Do you really need to know when? We don’t want to get off on a rant here but…Doesn’t the Boy Scout motto apply, no matter when? Be Prepared.

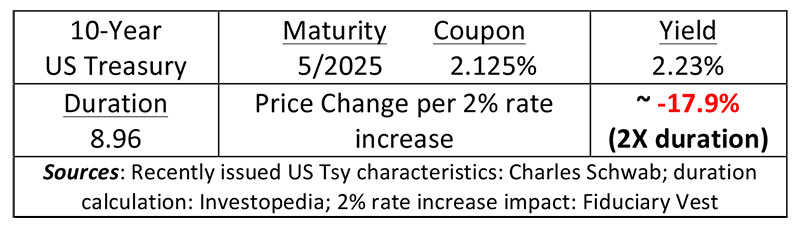

Bonds may not imminently prove the oft-predicted train-wreck from current low yields-longer duration, but does anyone think they are a good value, using the characterisitcs of the 10-Year Treasury (below) as a proxy?

While equities may not be expensive (only knowable for sure retroactively), it is hard to argue they look cheap from here – six years into price recovery, with peak company corporate profitability, high multiples, and low expected GDP/top line revenue growth.

Baseline equity returns combine current dividend yield PLUS an assumed 4% earnings growth (generously twice the average post-crisis GDP growth). Changes in P/E ratios are the lever that alter prospective returns, often significantly. Recent P/E readings for the S&P 500 were in the low 20s, against a long term average of 15.5. Further expansion which would boost earnings growth to better than 6% returns for investors is of course possible. Is it likely? Should investors count on it? We’re just asking.

Sources: S&P 500 est. yield: Yahoo Finance; P/E multiple and history: Multpl.com

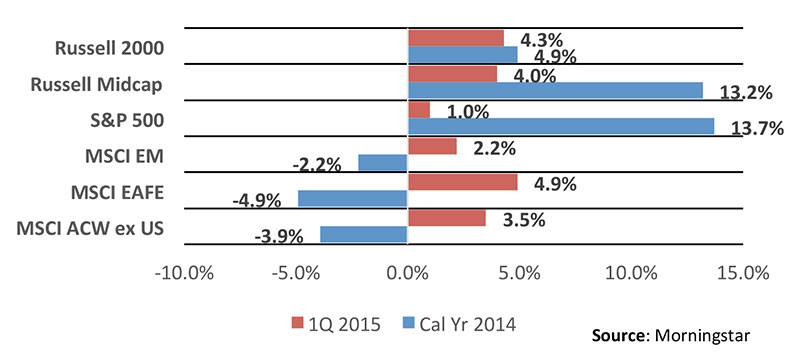

We’ve noticed of late a few directional indicators, in no particular order. Anecdotal: We read with interest that social networks are purported to house nascent and under-recognized stock market geniuses.9 Apple was recently added to the Dow Jones Industrial Average (one year return through 5/8/15 = 54.2%; 10 year = 38%, compounded), and uber-investor Warren Buffett (among others) said recently that if he could efficiently short a basket of corporate debt in size he would do so. Empirical: The growth investing style has been recently trouncing value, across the company size spectrum, often a late-cycle market behavior. We also note that the momentum orientation of passive benchmarks has them ascendant in a number of asset classes. Active management, tending toward more equally- than cap-weighted portfolios has consequently struggled in the partial market cycle which has lacked corrections of either significant duration or magnitude.

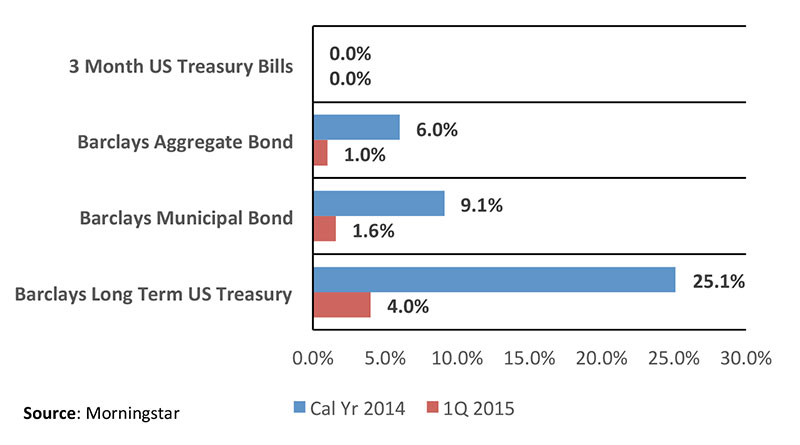

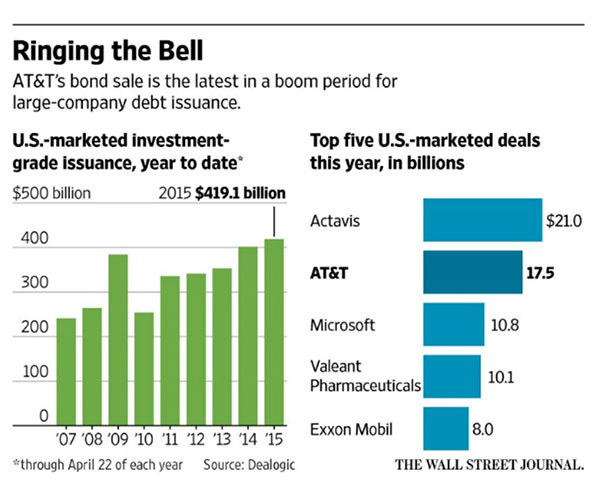

It is widely reported that investor margin balances – borrowing from brokers – are historically high, debt issuance is gargantuan (see graphic below), and of course the NASDAQ pushed past its pre-tech-crash 5000 peak (it only took fifteen years, with notably different constituents, we might add.)

One final signpost: airline stocks (arguably Warren Buffet, at% returnse in the low 20s,the Oracle of Omaha’s investing nemesis10) are on a tear and (gasp) breeding startup longevity in the notoriously competitive industry (the term Chapter 22 – Chapter 11, twice – may have been coined for it). Where but in bull-market America could one simultaneously witness both the resurrection of People’s Express (affectionately known as People’s Distress back in the day) and flight crews right out of Mad Men, complete with pencil skirts and pill-box hats?

Does any of this tell us stocks are too expensive? Sadly, no. Cheaper than before doesn’t mean “buy” and more expensive than before doesn’t mean “sell.” Note that Alan Greenspan waxed eerily rhapsodic to Ms. Yellen on the stock market and its possible “irrational exuberance” in December 1996 with the S&P 500 at 740; you may recall it had quite a way to go – in duration and amplitude – from there. Mr. Buffett proffered his view at his recent Berkshire Hathaway annual meeting that, if interest rates stay this low for a while, (emphasis ours) equities in today’s range will look like they were attractively priced. If forced to choose, we’d vote with the billionaire investor over the trained economists in this debate.

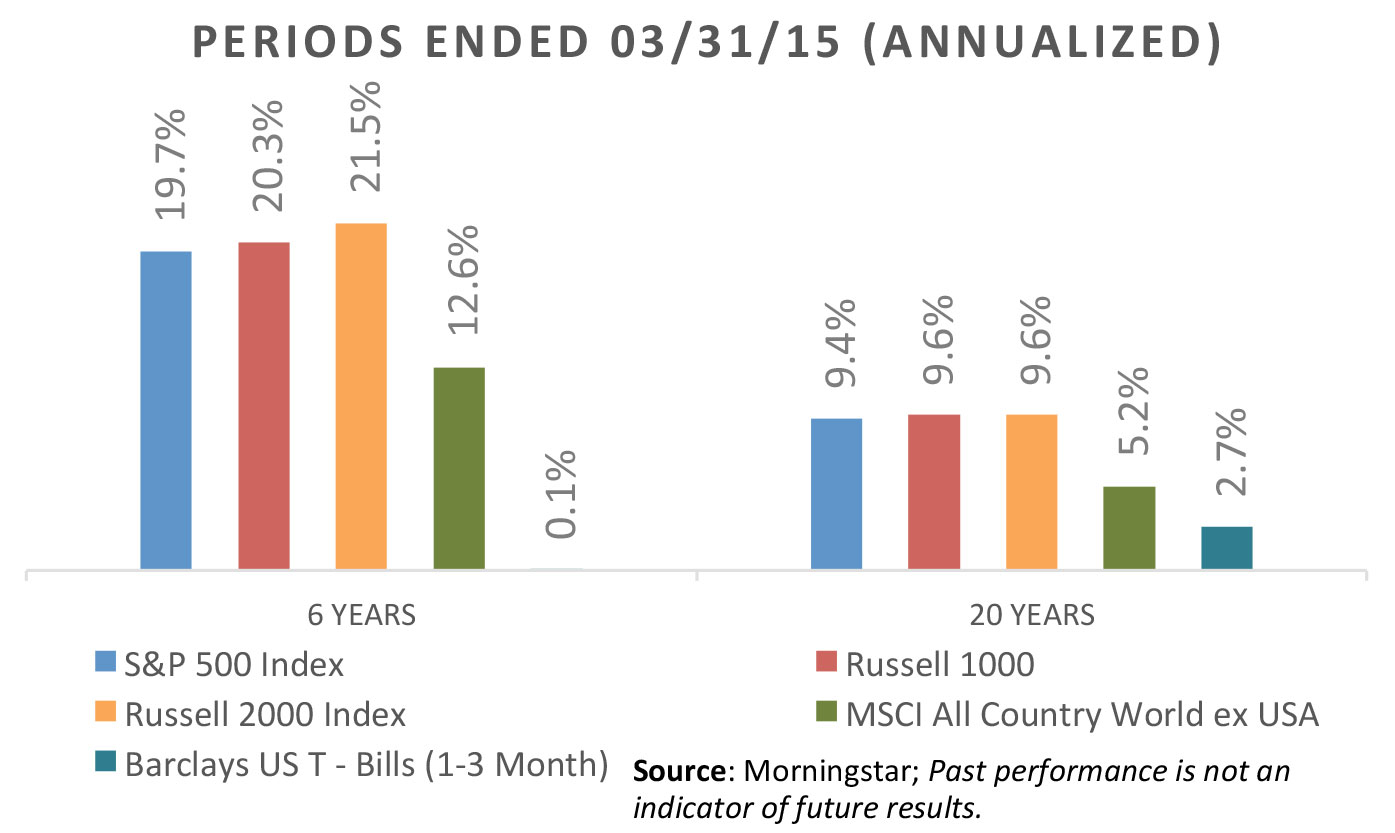

But If you believe in mean reversion (and we do), you should also prepare for and expect lower nominal returns from risky assets than those we’ve gotten used to since 2009. Long term, from here, lower nominal returns from stocks across the size specturm are just about a sure thing, especially in the US – see below. Of course that’s just our opinion; we could be wrong.

- Google reports she hates the nickname; apologies, Madonna, if you are a reader.

- America’s Smartest Business Woman? (FYI – Forbes asked the question – on their cover – not us; please hold any feminist ire!)

- Perhaps she later, er, repented – prior to Like a Prayer, anyway – and went tangible with 1987s remake of Santa Baby, with its appeals for fur, deeds, metals, and jewels. But we digress.

- What is Quantitative Easing?

- See our March Investment insight – What’s Another Trillion Among Friends?

- Unlike Draghi, Investors See a Point in Selling Euro; € Exchange 8/2/12 = $1.22 5/8/15 = $1.12

- Grift n. slang – A swindle or confidence game. IMDB.

- AZ-Lyrics

- Retail Traders Wield Social Media For Investing Fame.

- From a 2002 interview with the London’s The Telegraph: “…the airline business has been extraordinary. It has eaten up capital over the past century like almost no other business because people seem to keep coming back to it and putting fresh money in. You’ve got huge fixed costs, you’ve got strong labor unions and you’ve got commodity pricing. That is not a great recipe for success. I have an 800 (free call) number now that I call if I get the urge to buy an airline stock. I call at two in the morning and I say: ‘My name is Warren and I’m an aeroholic.’ And then they talk me down.”

Copyright ©2015, FiduciaryVest, LLC; all rights reserved.

This publication is NOT intended, or suitable as a basis for investment decisions. Before taking any significant action, readers should seek professional investment advice that will incorporate their specific investment needs and circumstances.