Saying Goodbye to Two1 (Heavy Sigh) Music Legends… and Central Bank Credibility?

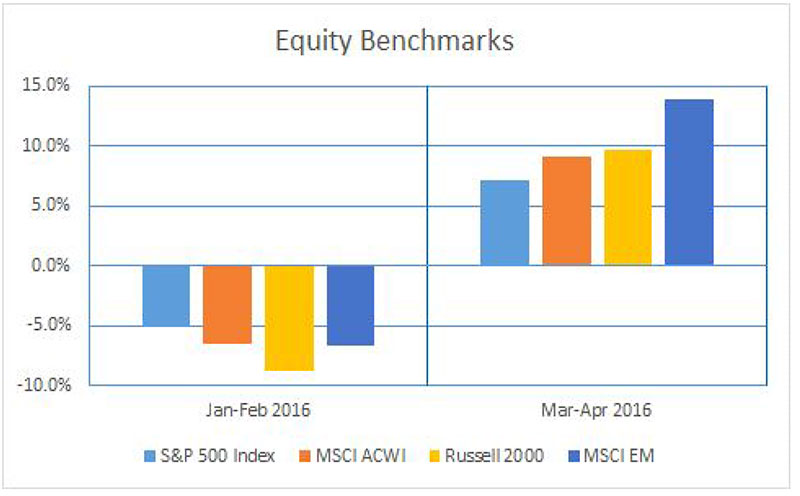

Demonstrating once again that capital markets are hyper-focused and likely unduly influenced by monetary policy, witness the bifurcation in returns during 2016 to date. Markets opened the year spooked by weak oil prices and shaky global economic data, especially out of China, but by nothing more so than December’s Fed Funds rate hike and (then) stated expectations. The Fed’s “four hikes in 2016” idea was already gone by February (lately odds are down to expecting two later this year) and markets reversed course, leaving stocks globally about where they began the year.

Generally, markets have tracked two data points in 2016: the price of oil and sentiment surrounding interest rate hikes. The early year swoon dovetailed plunging crude and hawkish Fed talk. I can’t tell you why oil and stocks should be positively linked, but risk assets recovered robustly from mid-February on. Because at the Fed, when doves cry, rate hikes become more distant… and the riskiest assets responded like a little red corvette.

Editorial Side Note: given that election year rate hikes are generally known to be wildly unpopular with incumbent parties of 1600 Pennsylvania Avenue’s resident, our guess on rates for 2016: When you’re down, that’s where you’ll stay .

You can check out any time you like, but you can never leave…

A renewed zeal for normalized, non-zero interest rates in the US was expected to be the new kid in town for 2016. A desperado January in markets, however, seems to have convinced the Fed that it cannot yet come down from its zero(ish) interest rate fences without some heartache tonight.

A renewed zeal for normalized, non-zero interest rates in the US was expected to be the new kid in town for 2016. A desperado January in markets, however, seems to have convinced the Fed that it cannot yet come down from its zero(ish) interest rate fences without some heartache tonight.

Basically, central banks said take it to the limit after the 2008 crash – 0% rates (negative in many countries) – and now even that isn’t good enough. After the thrill is gone, monetary policy theorists are finding that, it’s awfully hard to leave free money. And so you get ideas like those below being mooted, apparently without embarrassment:

- One idea that has attracted significant attention recently is direct transfers from the central bank to individuals and firms, often known as ‘helicopter money’.”

- “Whether central banks could cancel their government debt holdings is unclear. Any write-down in their value would wipe out the central bank’s capital2.” (What would we do without experts?)

- And then there’s our personal favorite from Donald Trump, the Monty Hall of American presidential politics: “I would borrow, knowing that if the economy crashed, you could make a deal” (on whether or not to pay US debts in full).

Who is gonna make it?, we’ll find out in the long run…In the long run, we’re all dead.

– JM Keynes, The Eagles

Maybe the powerful in Manhattan, Washington, Brussels, and Tokyo are too busy being fabulous to notice, but in a rational economic world, handing out free money and various forms of debt default by major nations qualify as bizarre, fringe, radical ideas – on par with free everything for everyone – that violate the price signals that market capitalism requires for good working order. How out there are we? Well, in our view, the next step just might involve Fed Chair Janet Yellen in a raspberry beret (the kind you find in second-hand store). And if it’s warm… well, let’s just not go there.

So what?, you might ask. Why does all this macro-talk matter? Don’t long-term investors do okay eventually? Yes, we still believe in basic long-term investing principles – goal setting, risk management, diversification, portfolio rebalancing, heck why not mom and apple pie too? We’ve got plenty of good tools to manage assets that maintain their appeal.

Nonetheless, we do periodically question just how much distortion the current take it easy policies are having on capital market outcomes. How much of the future’s returns have been fast-forwarded and will the hangover be like one too many glasses of Riesling, or more of a Tequila Sunrise? Are new crisis seeds already sprouting – not the 2013 “taper tantrum” variety, but more the two-thousand zero-zero, party over, it’s outta time type?

The world is awash in debt31, recovery or no recovery, and US corporate profits peaked in late 2014, with little valuation adjustment since then. All this while the world’s largest economy is in the midst of a presidential election where each “side” seems to believe of the other presumptive candidate: you can’t hide you’re lyin’ eyes. The campaign environment to date does not foster a peaceful easy feeling nor suggest fertile ground for the structural reforms needed to take some of the burden for recovery and economic growth off of monetary authorities as the last resort.

Though we’ve heard it said that you don’t have to watch Dynasty to have an attitude, we nonetheless offer advance apologies for the profusion of prose vs. graphics, and for the purple rain tone of our thoughts. In summary, we just can’t help but feel like there’s trouble on the street tonight, or if you prefer a Game of Thrones metaphor, that winter is coming. In our view, even if they just learn to be still, investors should avoid life in the fast lane or else end up in the sad café one of these crazy old nights. Thanks for reading – we’re told at least one fan has been awaiting this release; hopefully someday we will find that it wasn’t really wasted time.

- Rest in Peace Glenn Frey and Prince Rogers Nelson. We aren’t (necessarily) wed to music quotes to frame our market observations, however, the 2016 passing of so many1 legends just seems to invite the usage.

- What are the style rules on footnoting a footnote? At any rate, we’ve now lost David Bowie, Glenn Frey and, most recently, Prince all in just the first half of 2016. Proving that Warner Brothers retains Bugs Bunny’s wise guy bona fides to this day, a recent episode of Wabbit featured a Grim Reaper character, stalking Bugs, being distracted by “Look, Keith Richards.” With all due respect to another legend, Keith might want to keep a personal physician on stage during the Stones pending tour. But we digress.

- McKinsey Global Institute: Debt And (Not Much) Deleveraging, February 2015

- Six years after a crisis caused by excessive borrowing, McKinsey estimates that even visible global debt has increased by $57 trillion, while in the U.S., Europe, Japan and China growth to pay back these liabilities has been slowing or absent.

Editor’s Note: Prizes are available for those who correctly identify the number of Eagles / Prince song titles / lyrics embedded within.

Copyright © 2016 FiduciaryVest, LLC; All rights reserved.

This publication is not a suitable basis for investment decisions.